Table of Contents

What is inflation?

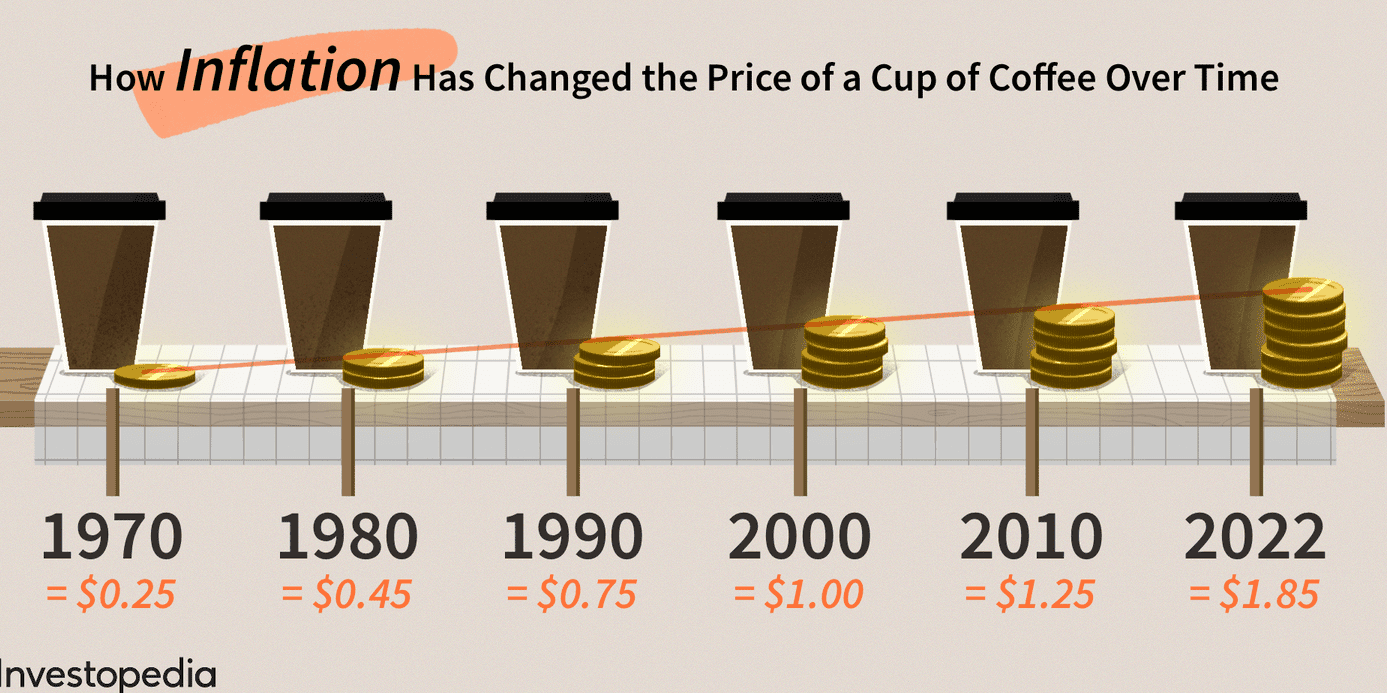

Ever heard your grandparents talk about how everything was so much cheaper back in their day? They might say things like, “In the 1960s, 10 grams of 24 karat gold was just Rs. 65!” Well, guess what? That same gold now costs a whopping Rs. 48,530. What happened? Inflation happened. Let’s dive into this sneaky thief that makes our money worth less over time and figure out how to beat it.

Inflation is like gaslighting on a grand scale. Imagine someone telling you that things aren’t actually getting more expensive because everything else is also getting more expensive. It’s like they want you to believe that you’re not drowning because everyone else is sinking too!

The Rat Race

It’s like running on a rat wheel. If you speed up, you might get a little ahead of the pack. But if everyone starts running faster, nobody actually gets ahead. The wheel just spins faster and faster. You make more money, but everything else gets more expensive. Your rent, insurance, and bills all go up. The faster you run, the faster the wheel spins, draining your bank account quicker.

Cricket Bat Example

Let’s use a cricket bat to illustrate this. Five years ago, you bought a good-quality cricket bat for $100. Today, you go to buy the same bat, and it costs $120. Here’s how inflation plays into this:

- Price 5 Years Ago: $100

- Price Today: $120

To find the inflation rate:

- Inflation Rate = [(Current Price – Initial Price) / Initial Price] * 100

- Inflation Rate = [($120 – $100) / $100] * 100

- Inflation Rate = 20%

So, over five years, the price of the cricket bat increased by 20%. Now, you need $120 to buy the same bat that cost $100 five years ago. Inflation makes your money worth less over time, making everything more expensive.

Inflation in India: The Two Big Indices

- Wholesale Price Index (WPI): Measures price changes at the wholesale level – think of it as the bulk prices businesses pay.

- Consumer Price Index (CPI): Measures price changes at the retail level – what you and I pay at the store.

Causes of Inflation

- Demand-Supply Gap: Too many people want something that isn’t being produced enough. Think of a Black Friday sale with only 10 TVs on discount.

- Too Much Money Circulation: When there’s too much money floating around, it loses value.

- Increased Spending: When people have more money, they tend to spend more, driving prices up.

Effects of Inflation

- Industrial Sector: Higher prices for raw materials and labor squeeze companies’ profit margins. Eventually, they pass these costs to us, the consumers.

- Buying Power of the Rupee: As prices rise, the rupee buys less. That’s why folks in India might get salary hikes of 15–30% annually, while in the US, the average hike is around 3%.

- Decrease in Investments: Inflation can scare off both local and international investors because it makes financial planning tricky.

How to Beat Inflation

- Invest in Equities and Mutual Funds: These can offer returns that outpace inflation.

- Buy Real Estate or Gold: These are tangible assets that typically increase in value over time.

- Diversify Globally: Different countries have different inflation rates, so spread your investments around.

Is Inflation Always Bad?

Surprise! Inflation isn’t always a villain. A little bit of inflation (around 2%) can actually help the economy grow. It encourages people to spend rather than hoard money. But when inflation goes above 3%, it usually spells trouble.

The Hyperinflation Horror Story: Zimbabwe

Zimbabwe is the poster child for what happens when inflation goes wild. The Zimbabwean government decided to solve its economic problems by printing more money. The result? Hyperinflation. Prices went up so fast that a loaf of bread could cost billions of Zimbabwean dollars.

At its worst, Zimbabwe’s inflation rate hit 79,600,000,000% per month in July 2008. Eventually, they had to abandon their currency and switch to US and South African currencies. To mop up the old Zimbabwe dollars, they offered an exchange rate of $1 for 35 quadrillion Zimbabwean dollars. Yes, you read that right—quadrillions! (boombastic side-eye)

The Takeaway

Inflation is like that sneaky thief you don’t notice until your pockets are empty. It’s why your grandparents’ stories of cheap goods sound like fairy tales. By understanding inflation and investing wisely, you can protect your money from losing its value over time.

So, keep an eye on inflation, stay smart with your money, and you won’t end up feeling like you’re living in a bad hyperinflation horror movie!

For more tips on money management and personal finance, follow my blog! Because if you’re not wiser with your money, you might just end up being a miser.

FAQs

What do you mean by inflation?

Inflation is the rate at which the general level of prices for goods and services rises, eroding purchasing power. In simple terms, it means that over time, money buys less than it did before. If inflation is 2%, something that costs $100 today will cost $102 next year.

What causes inflation?

Inflation can be caused by several factors, including:

- Demand-Pull Inflation: When demand for goods and services exceeds supply, prices rise.

- Cost-Push Inflation: When production costs increase (like higher wages or raw material costs), businesses raise prices to maintain profit margins.

- Built-In Inflation: When people expect prices to rise, they might demand higher wages, which can lead to higher costs and prices.

Is inflation good or bad?

Inflation has both positive and negative effects. Moderate inflation can be beneficial as it encourages spending and investing rather than hoarding cash. However, high inflation can erode purchasing power and lead to economic instability. Balancing inflation is key to economic health.

What is India’s current inflation rate?

As of the latest data, India’s inflation rate fluctuates, typically ranging between 4% to 6%. For the most accurate and up-to-date figure, check recent reports from the Reserve Bank of India or government statistics.

Is inflation good for the rich?

Inflation can benefit the rich if their assets (like real estate or stocks) increase in value faster than the inflation rate. However, inflation can also erode the value of cash holdings and fixed-income investments, impacting wealth in different ways.

Who benefits from inflation?

Borrowers often benefit from inflation because the real value of their debt decreases over time. If inflation is higher than expected, the money they repay is worth less than when they borrowed it. Asset holders, like property owners or stock investors, can also benefit if their investments appreciate in value.

Who loses from inflation?

People with fixed incomes or cash savings are often hurt by inflation, as their purchasing power diminishes. Retirees relying on fixed pensions or savings accounts may find that their money buys less over time. Additionally, inflation can disrupt business planning and erode profit margins if companies can’t pass higher costs onto consumers.

Why is low inflation good?

Low inflation is generally good because it indicates a stable economy. It allows consumers to make long-term plans, helps maintain purchasing power, and avoids the economic distortions associated with high inflation. It also makes it easier for businesses to set prices and for consumers to budget.

Why is 2 percent inflation good?

A 2% inflation rate is often considered ideal because it reflects a stable and growing economy. It provides a cushion against deflation (falling prices), encourages spending and investing, and is generally manageable for both consumers and businesses. Central banks, like the Federal Reserve, target around 2% inflation to promote steady economic growth while avoiding the pitfalls of higher inflation.

Latest episodes

Leave a Reply