Table of Contents

What is Blockchain?

Imagine a big, super-secure digital notebook that everyone can see, but no one can change. That’s blockchain! Every time someone writes down a transaction, it’s signed to make sure it’s real and can’t be tampered with. This technology is set to change a lot of things in various industries.

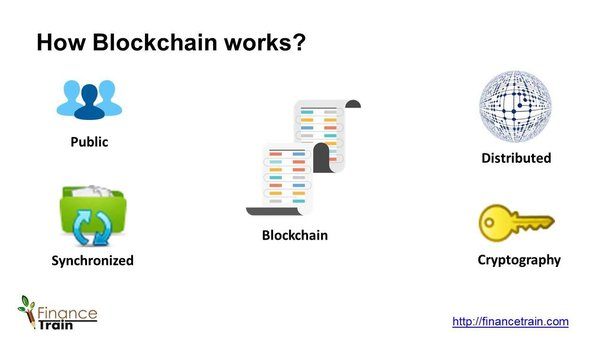

How Does Blockchain Work?

Three main parts make blockchain work:

- Private key cryptography:

Two people wish to transact over the internet.

Each of them holds a private key and a public key.

The combination of these keys can be seen as a dexterous form of consent, creating an extremely useful digital signature.

While authentication is solved, it must be combined with a means of approving transactions and permissions (authorization).

2. A Distributed Network: The benefit and need for a distributed network can

be understood by the ‘if a tree falls in the forest’ thought experiment.

If a tree falls in a forest with cameras to record its fall, we can be pretty certain that the tree fell. We have visual evidence, even if the particulars (why or how) may be unclear.

In short, the size of the network is important to secure the network.

3. System of record:

When cryptographic keys are combined with this network, a super useful form of digital interactions emerges. The process begins with A taking their private key, making an announcement of some sort — in the case of bitcoin, that you are sending a sum of the cryptocurrency — and attach it to B’s public key.

4. Network servicing protocol: The type, amount and verification can be different for each blockchain. It is a matter of the blockchain’s protocol – or rules for what is and is not a valid transaction, or a valid creation of a new block. The process of verification can be tailored for each blockchain. Any needed rules and incentives can be created when enough nodes arrive at a consensus on how transactions ought to be verified.

It’s a taster’s choice situation, and people are only starting to experiment.

We are currently in a period of blockchain development where many such experiments are being run. The only conclusions drawn so far are that we are yet to fully understand the dexterity of blockchain protocols.

Example, The Group of Friends

Imagine a group of 12 friends named January through December. These friends are honest and never lie. They have a ritual of sharing everything happening to them over a walkie-talkie network, ensuring no information is ever lost or forgotten.

For instance, if September gives a rose to April on Valentine’s Day, everyone in the group will know about it. This means neither September nor April can deny this event later because everyone heard the broadcast. Similarly, if June buys an iPhone from January for $100, and later tries to sell it to August claiming it’s brand new, August will know it’s not true because he heard about the sale a year ago. Every friend in the group can confirm this information because they all remember it accurately.

This network of friends is akin to a blockchain network. Each friend represents a node that stores information. Once a piece of information is shared, it cannot be changed or deleted. This creates a system where lying or manipulating data is nearly impossible because it would require convincing the majority of the group to go along with the lie.

Centralized vs. Decentralized Systems

Now, imagine if January was the leader and the sole keeper of all information. If January decides to lie, manipulate data for personal gain, or loses the data, the system fails. This centralized approach poses several risks:

- January could lie for personal benefit.

- Data could be lost if January’s record is compromised.

- Secrets could be stolen from January.

- January could be corrupted, making it easier to manipulate one person rather than the whole group.

- If January leaves the group or dies, all information would be lost.

To address these issues, blockchain technology was developed. Instead of a central authority, blockchain uses a decentralized network where every participant stores and verifies transactions. This makes the system more trustworthy and secure.

The Mechanics of Blockchain

In a blockchain network, every transaction is recorded across multiple nodes (computers, laptops, mobile phones, etc.). This replication ensures that if one node fails, the data is still available on other nodes, eliminating single points of failure. Every transaction is approved by a majority, ensuring its validity. This is similar to how a group of friends would need the majority to confirm a piece of information.

Blockchain’s decentralization offers several benefits:

- Increased trust as everyone has the complete history of transactions.

- Fraud prevention as any false information can be disproven by the majority.

- No single point of failure, ensuring robustness.

- Continuity even if some participants leave the network.

- Difficulty in manipulating a large, decentralized group compared to a single entity.

Blockchain in Action: The Example of Money

Let’s extend this understanding to financial transactions. Imagine you’re a singer who records a song and shares it online. The song can be duplicated endlessly, which is great for sharing files but not for money. If you send $10 to a friend, you shouldn’t still have that $10. Blockchain ensures that once money is spent, it cannot be duplicated.

Unlike traditional systems like PayPal or banks, blockchain has no central regulator. Instead, all users collectively act as auditors. This eliminates intermediaries and their fees, making transactions faster and cheaper. For example, sending money from Korea to Russia traditionally involves banks, currency conversions, and high fees. Blockchain simplifies this by enabling direct transactions, saving time and money.

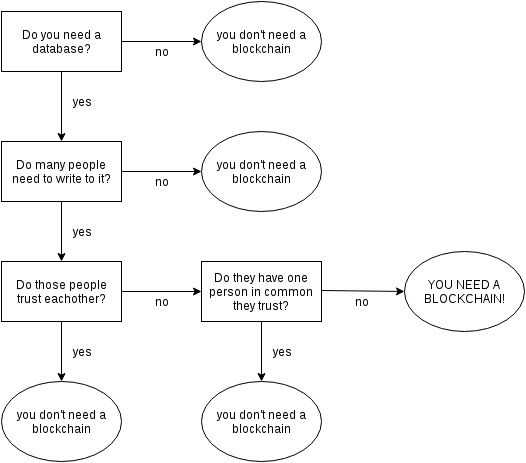

Do you need a block chain?

Many people try to use blockchain to solve problems that are much better solved with simpler technologies.

So where can block chains actually be used?

| Use Case | Applications |

|---|---|

| Cryptocurrencies | Bitcoin, Ethereum |

| Cross-border Payments | International money transfers |

| Supply Chain Management | Tracking products, Food safety |

| Healthcare | Patient records, Drug traceability |

| Voting Systems | Secure voting, Voter verification |

| Real Estate | Property transactions, Title management |

| Digital Identity | Identity verification, KYC processes |

| Intellectual Property | Copyright protection, Patent management |

| Charity and Donations | Transparent donations, Non-profit accountability |

| Legal and Smart Contracts | Automated contracts, Legal document management |

| Education | Credential verification, Student records |

| Government Services | Land registry, Public records |

Blockchain technology is changing how we record and verify transactions. It’s a secure, transparent, and decentralized alternative to traditional systems. This technology is being used in many sectors, like finance, retail, manufacturing, and healthcare, promising a future where trust and efficiency are key.

Understanding blockchain with simple examples makes it easier to see how it works and its potential to change how we handle information and transactions.

FAQs

1. What is blockchain in simple words?

Blockchain is like a digital ledger that records transactions across many computers in a way that ensures security and transparency. Think of it as a book where every page (block) is connected (chain), and once a page is written, it can’t be changed.

2. What is the main purpose of blockchain?

The main purpose of blockchain is to provide a secure, transparent, and decentralized way to record transactions. It eliminates the need for intermediaries, reduces fraud, and ensures that data cannot be tampered with.

3. What is a blockchain for beginners?

For beginners, blockchain is a system of recording information in a way that makes it difficult or impossible to change or hack. It is essentially a digital ledger of transactions that is duplicated and distributed across a network of computer systems.

4. What is blockchain vs cryptocurrency?

Blockchain is the technology that underpins cryptocurrencies. It is a method of recording data. Cryptocurrency, like Bitcoin, is a type of digital or virtual currency that uses blockchain technology to secure and verify transactions.

5. Is Bitcoin a blockchain?

Bitcoin is not a blockchain; it is a cryptocurrency. However, it was the first and is the most well-known application of blockchain technology, using it to enable secure and decentralized transactions.

6. Who invented blockchain?

Blockchain technology was first conceptualized by an unknown person or group of people using the name Satoshi Nakamoto in 2008 to serve as the public transaction ledger of the cryptocurrency Bitcoin.

7. Who is the owner of blockchain?

No one owns blockchain technology. It is a decentralized and open-source system, meaning it is maintained by a distributed network of computers worldwide rather than any single entity or individual.

8. Who really owns Bitcoin?

The true identity of Bitcoin’s creator, Satoshi Nakamoto, remains unknown. Various individuals and entities own Bitcoin, but the largest known holder is Satoshi Nakamoto, who is estimated to possess around 1 million Bitcoins.

9. Who is the richest Bitcoin owner?

The richest Bitcoin owner is believed to be its mysterious creator, Satoshi Nakamoto, with an estimated 1 million Bitcoins. Among known individuals, figures like the Winklevoss twins, who invested early in Bitcoin, hold significant amounts.

Latest episodes